How to Know You’re Ready to Buy a Home

Buyers February 10, 2025

Buyers February 10, 2025

Buying a home is a big decision, and knowing when you're truly ready can feel overwhelming. While there’s no one-size-fits-all answer, there are several key indicators that signal you might be prepared to take the next step toward homeownership. If you’re wondering whether now is the right time, here are five factors to consider.

1. You Have a Stable Income

A steady and reliable income is one of the most important factors when considering homeownership. Lenders typically look for at least two years of consistent employment in the same field or industry. If you have:

…you might be in a good position to buy a home.

2. You’ve Saved for a Down Payment and Closing Costs

Contrary to popular belief, a 20 percent down payment isn’t always required. Many first-time homebuyer programs allow for as little as 3 to 5 percent down, but additional costs, such as closing fees and moving expenses, should also be factored in.

What to Budget For:

3. Your Credit Score is in Good Shape

Your credit score plays a significant role in determining the mortgage rates available to you. While some lenders accept scores as low as 620, a higher score (typically 700 or above) can help secure a better interest rate, reducing your monthly payments.

How to Check If Your Credit is Mortgage-Ready:

If your score needs improvement, paying down debts and avoiding new credit inquiries can help strengthen your financial position before applying for a mortgage.

4. Your Debt is Under Control

Lenders evaluate your debt-to-income ratio (DTI) to determine if you can afford a mortgage. This ratio compares your total monthly debt payments to your gross income.

Reducing debt before purchasing a home can improve your loan options and ensure financial stability once you become a homeowner.

5. You’re Ready for the Responsibilities of Homeownership

Unlike renting, owning a home means taking on maintenance, property taxes, and long-term commitments. Before buying, consider:

Final Thoughts

Deciding whether you’re ready to buy a home involves more than just finances—it’s about stability, future goals, and personal readiness. If you find yourself checking most of these boxes, homeownership could be the right next step for you.

Stay up to date on the latest real estate trends.

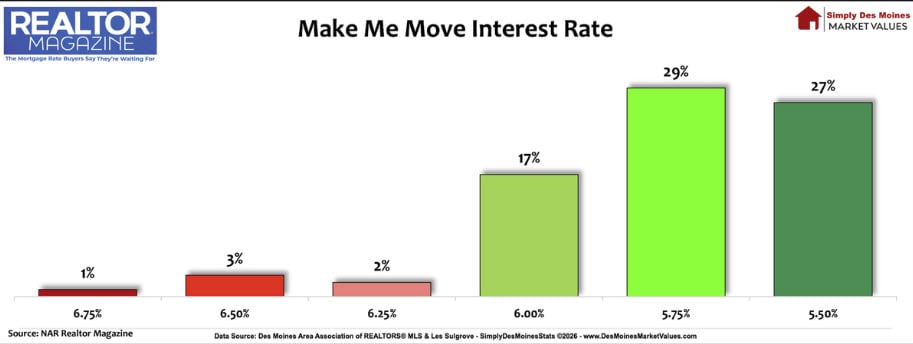

If you've been waiting to buy, now might be the time.

For the best service and results when it comes to all of your real estate needs, reach out anytime.