First-Time Homebuying In Urbandale: A Local Step-By-Step

February 19, 2026

February 19, 2026

Buying your first home in Urbandale can feel big, but it does not have to be confusing. You want a clear plan, local insight, and confidence that you are making smart choices. In this guide, you will learn each step in plain language, with Urbandale-specific tips on financing, neighborhoods, inspections, and closing. Let’s dive in.

Recent vendor snapshots place typical Urbandale home values in the mid-$300Ks, though estimates vary by data source and timing. Inventory and days to pending can shift by price band, with stronger competition at entry-to-mid price points and softer demand higher up. Use price bands to frame your search, for example: under ~$300k, $300k–$425k, and $425k+. Always confirm the latest MLS data with your agent before you make an offer.

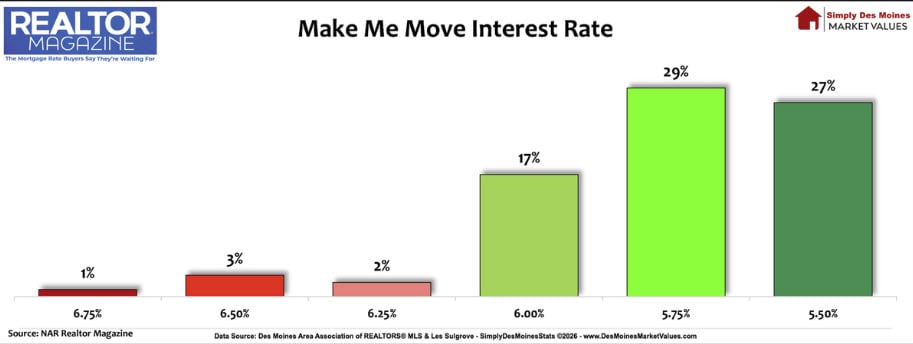

Start with a written pre-approval so you know your price range and can move fast. Bring a photo ID, recent pay stubs, and bank statements to your first lender meeting. If you plan to use Iowa first-time buyer assistance, choose a lender who participates in Iowa Finance Authority programs like FirstHome or FirstHome Plus. You can review program details on the Iowa Finance Authority’s FirstHome Plus page at Welcome Home Iowa.

Many first-time buyers in Iowa use IFA assistance to reduce cash to close. Depending on eligibility, programs can provide a $2,500 grant and, in some cases, a 0% second loan up to the lesser of 5% of price or $5,000 for down payment or closing costs. Income and purchase price limits apply by county, and homebuyer education is typically required. Check current rules and confirm your eligibility with an IFA-participating lender.

Expect more than the principal and interest payment. Property taxes, homeowners insurance, and HOA dues if applicable can add a meaningful amount each month. The U.S. Census QuickFacts for Urbandale lists local owner cost and value figures, which can help you set a realistic budget. Review the Urbandale data on Census QuickFacts, and consider the homestead credit process with the Polk County Assessor. For tax specifics, confirm details with the Assessor or a tax professional.

If schools are part of your decision, start with the Urbandale Community School District’s official resources. The district posts registration dates, calendars, and links to boundary information. Always verify attendance boundaries for a specific address with the district. Review current updates from the Urbandale Community School District.

Urbandale’s mean commute time is under 20 minutes according to Census QuickFacts. Do a test drive to and from your workplace at peak times to compare options. Also note that many Urbandale neighborhoods include single-family detached homes, with a mix of mid-century houses and newer subdivisions. Expect a range of basement styles, typical suburban lots, and a variety of finishes.

If you plan multigenerational living or potential rental income, review Urbandale’s accessory dwelling unit standards. The city permits one ADU per single-family lot with size and setback limits. Read the ADU section of the Urbandale municipal code and contact Community Development for permits and next steps.

A strong offer package includes your pre-approval letter and proof of funds for earnest money. Discuss earnest money with your agent before you submit. In the Des Moines metro, many first-time buyers offer $1,000–$3,000 on entry-to-mid price homes, while some raise the deposit to around 1%–2% in more competitive cases.

Build in smart protections. Inspection, financing, and appraisal contingencies are common tools to manage risk. A 7–10 day inspection window is a common starting point in many Midwestern contracts, but your agent will confirm the local standard and draft terms that fit your situation. Budget for add-ons like radon testing, sewer scope, pest inspection, or well/septic checks if they apply to the property.

Plan to test for radon. Polk County and most of Iowa fall in the EPA’s Radon Zone 1, which signals the highest potential for elevated indoor levels. Include a short-term radon test during your inspection period and, if levels are high, discuss mitigation with your inspector and agent. See the EPA radon map for context.

Check floodplain overlays and drainage patterns. Urbandale has a floodway and floodway fringe overlay in the zoning code, so review the map and standards when a home sits near waterways. Ask about past water intrusion, sump pump history, and any drainage improvements during your showing and inspection. For local rules, see the city’s Floodway Fringe section.

Understand seller disclosures. Iowa law requires a property condition disclosure for most 1–4 unit residential transfers, and timing matters. The disclosure must be delivered before you accept an offer or you may have a short rescission window. Review the Iowa Real Estate Commission’s rule notice for context on delivery and content at rules.iowa.gov. Homes built before 1978 also require federal lead-based paint disclosures.

Set expectations for cash to close. Buyer closing costs in many markets run about 2%–5% of the purchase price. Your lender’s Loan Estimate will outline fees early, and you should receive a Closing Disclosure at least three business days before settlement. For a helpful overview of typical fee categories, see this summary of common closing costs.

Know who does what at closing. In Urbandale, title and settlement companies handle escrow, title insurance, and recording. Fees vary by county and company, and who pays for the owner’s title policy can differ by local custom. Ask your title company for a fee sheet and check recording details with Polk County.

Plan your timeline. Days to pending in recent months often fall in the 40–50 day range depending on price point and season, and your financing timeline can shape the close date. After acceptance, the usual sequence is inspection, appraisal, final underwriting, then closing. Many financed deals close in about 30–45 days, while cash can be faster.

As a first-time buyer, your best advantage is a clear plan and a local team that knows Urbandale block by block. If you want a calm, step-by-step process and straight talk on neighborhoods, pricing, and offers, we are here to help. Connect with Boutique Real Estate (Iowa) to start your search and move forward with confidence.

Stay up to date on the latest real estate trends.

If you've been waiting to buy, now might be the time.

For the best service and results when it comes to all of your real estate needs, reach out anytime.