The "Make Me Move" Rate... and Why This Is Getting Interesting

Kristin Coffelt March 9, 2026

Kristin Coffelt March 9, 2026

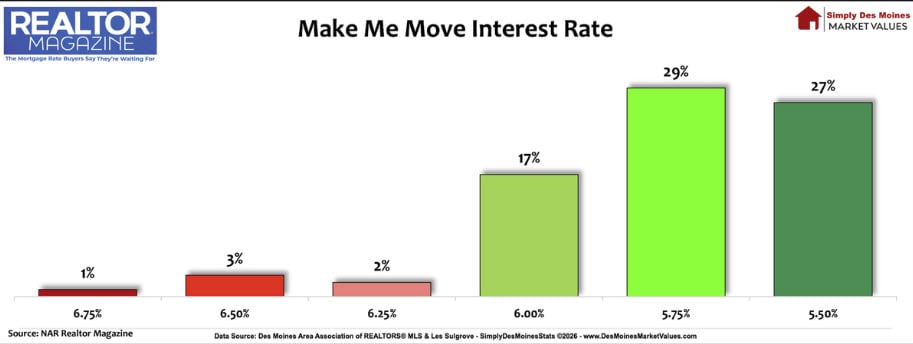

Last summer, buyers were asked a simple question:

“At what interest rate would you finally feel ready to move?”

The answers weren’t dramatic. They were practical.

Around 6%, people said, “Okay… this feels reasonable.”

But when rates hit 5.5% to 5.75%, nearly two-thirds of buyers said,

“Alright. Now I’m ready.”

Now here’s the part that makes this conversation relevant:

Rates in the Des Moines metro are hovering around 5.49%.

We’re basically sitting in the zone buyers said they were waiting for.

And when that happens?

Buyers who’ve been watching from the sidelines start stepping back in.

Which raises the next question I hear all the time:

“Should I wait for rates to go even lower?”

I get the temptation. Everyone wants the lowest rate possible. But trying to perfectly time mortgage rates is like trying to perfectly time the stock market. It sounds smart in theory… and rarely works that way in real life.

Here’s what can happen:

You decide you’re waiting for 5.25%.

Rates drop to 5.35%.

The right house pops up.

You hesitate.

It sells.

And rates never quite hit your number.

Meanwhile, competition picks up because everyone else was waiting for the same thing.

The part people forget?

If rates drop after you buy, you can refinance.

But if rates rise after you wait, you’re stuck playing defense - against both other buyers and the bank.

The real strategy isn’t chasing the absolute lowest rate.

It’s understanding your payment comfort, your timeline, and what makes sense for your life.

If you’re wondering what 5.49% actually means for your buying power, let’s run the numbers. Sometimes seeing the real payment - not just the headline rate - makes the decision a lot clearer.

Stay up to date on the latest real estate trends.

If you've been waiting to buy, now might be the time.

For the best service and results when it comes to all of your real estate needs, reach out anytime.