Move Up Buyers in West Des Moines: Plan Your Next Step

March 12, 2026

March 12, 2026

Eyeing more space in West Des Moines but unsure how to juggle selling your current home and buying the next one? You’re not alone. Many homeowners want to move up without double moves, missed opportunities, or surprise costs. In this guide, you’ll get a clear read on today’s local market, side-by-side timing options, Iowa-specific closing steps, and practical timelines to help you plan with confidence. Let’s dive in.

West Des Moines prices are holding in the low-to-mid $300,000s in early 2026. Public trackers use different methods, so you’ll see a range, but the big picture is steady demand with more choices than a year ago. At the metro level, the Des Moines Area Association of Realtors reported 13,916 homes sold in 2025 and a median sales price near $315,000, with conditions shifting from very tight to more balanced late in the year. These metro trends often spill into West Des Moines and affect how realistic sale contingencies and rent-backs will be for your purchase. You can review the year-end snapshot in the DMAAR report for context on inventory and days on market. DMAAR’s 2025 housing stats

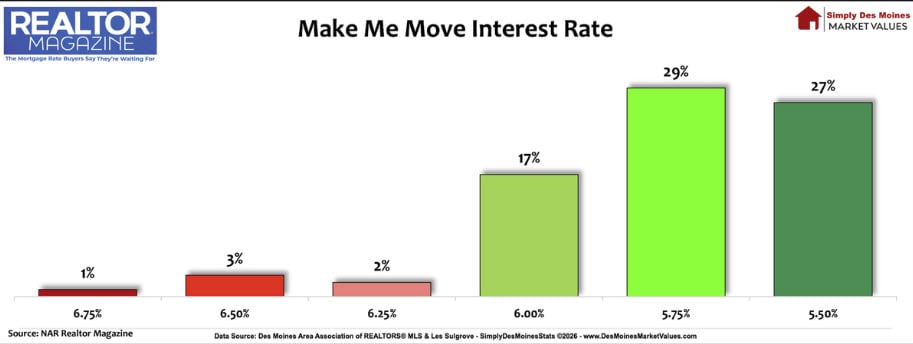

Mortgage costs shape affordability too. Freddie Mac’s weekly survey in early March 2026 showed 30-year fixed rates around 6 percent, and even small rate moves can change your budget and competitiveness. Freddie Mac Primary Mortgage Market Survey

Local changes can matter by submarket. For example, early March 2026 redevelopment plans around Valley West Mall could influence interest and timing near that corridor, while areas like Jordan Creek, Valley Junction, and newer subdivisions each have their own rhythm. Axios coverage of Valley West plans

Bottom line: Your best move-up plan depends on how quickly your current home will sell at market price, how much equity you can access upfront, and how competitive the target neighborhood and price band are.

Selling first gives you certainty on net proceeds and prevents carrying two mortgages. You’ll head into your next purchase with cash in hand and a stronger negotiating position. The tradeoff is arranging temporary housing or a short-term rental if the right home isn’t available right away. If your current home is likely to sell quickly, this path can be efficient and lower risk.

Buying first lets you shop without pressure and write a non-contingent offer, which can be more attractive to sellers in faster segments. You may need a bridge loan, HELOC, or other equity-access tool to cover your down payment before your sale closes, which adds cost and underwriting steps. Model a few months of worst-case carrying costs and work closely with your lender on debt-to-income impacts. Types of home equity financing

With a sale contingency, you write your purchase offer conditional on selling your current home by a certain date. Sellers often require you to list immediately and may add a kick-out clause that allows them to keep showing the home. If a stronger buyer appears, you typically get a short window to remove your contingency or step aside. This can be workable in more balanced segments but is still weaker than a non-contingent offer. NAR guide to contract contingencies

Iowa uses an abstract-and-attorney-title-opinion system supported by the state-run Iowa Title Guaranty program. Plan for an abstract update and attorney title opinion before the guaranty certificate is issued. Your title partner will coordinate these steps, but they affect timing, so build them into your schedule early. Iowa Title Guaranty overview

Typical purchase loans close in about 30 to 45 days, depending on appraisal, underwriting, and document turn times. Under federal TRID rules, you must receive the Closing Disclosure at least three business days before closing. If you plan back-to-back closings, set firm milestones and add buffer days to avoid last-minute surprises. Closing speed and TRID timing basics

Recording is handled by the Polk County Recorder. Confirm any local documentary requirements and recording cutoffs with your title company early, especially if you need funding and possession on the same day. Polk County recording information

In faster price bands with low days on market, non-contingent offers still have an edge. If you must use a sale contingency, list early, price to current comps, and be ready to remove the contingency quickly. In segments where inventory has improved and market times are longer, contingent offers and short rent-backs are more workable, though still less appealing to sellers than clean financing. Check metro stats for direction and calibrate by neighborhood, such as Jordan Creek, Valley Junction, and newer subdivisions. DMAAR’s 2025 housing stats

You can time a move-up in West Des Moines with less stress by pairing a clear offer strategy with Iowa-specific closing steps and a realistic calendar. If you want a step-by-step plan, market-tested pricing, and polished marketing for your sale, we’re here to help. Reach out to Boutique Real Estate (Iowa) to run your numbers, compare scenarios, and start your next chapter.

Stay up to date on the latest real estate trends.

If you've been waiting to buy, now might be the time.

For the best service and results when it comes to all of your real estate needs, reach out anytime.